Homeowners Insurance Homeowners Insurance 101

Homeowners Insurance is an essential safeguard for homeowners, providing financial protection against various risks associated with owning a home. This insurance typically covers the structure of the home, personal belongings, liability for injuries and accidents that occur on the property, and other financial losses. Understanding the nuances of homeowners insurance is vital for any homeowner to ensure they have adequate coverage and peace of mind.

When it comes to homeowners insurance, several key aspects deserve attention:

- What is Homeowners Insurance?

Homeowners insurance is a type of property insurance that provides financial protection against a range of potential risks that could result in loss or damage to your home and its contents.

- Coverage Types:

Homeowners insurance policies generally provide coverage in the following categories:

- Dwelling Coverage: This protects the actual structure of your home, including the walls, roof, and attached structures in the event of fire, theft, or significant weather events.

- Personal Property Coverage: This applies to your belongings within the home, such as furniture, electronics, and clothing, ensuring financial recovery in case of damage or loss.

- Liability Coverage: This protects you from legal claims and expenses that may arise if someone is injured on your property or if you accidentally damage someone else's property.

- Additional Living Expenses: If your home becomes uninhabitable due to a covered peril, this covers the costs of temporary lodging, meals, and other living expenses.

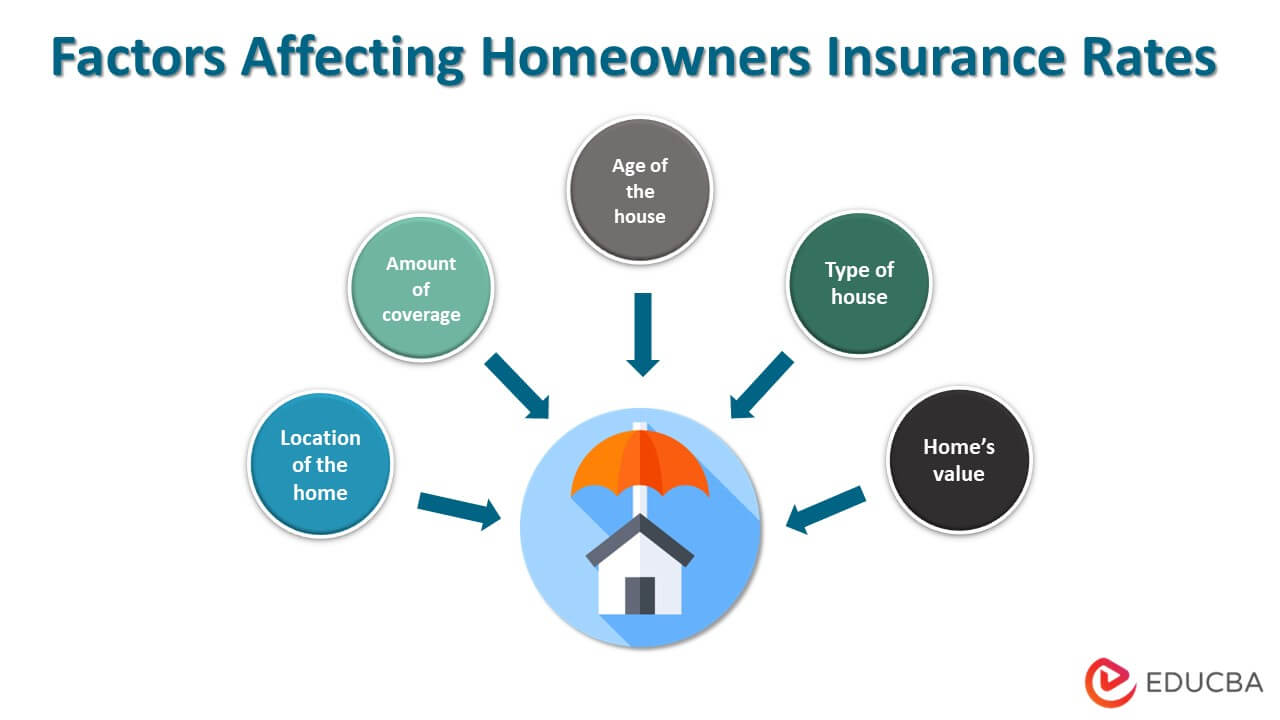

- Factors Influencing Premiums:

The cost of homeowners insurance premiums can vary widely based on several factors, including:

- The location of the home and its risk profile.

- The age and condition of the house.

- The coverage amount selected and the deductible.

- Your credit history and claims history.

- Common Exclusions:

While homeowners insurance offers broad coverage, it also contains exclusions that homeowners should be aware of:

- Flood damage typically requires a separate policy under flood insurance.

- Earthquake damage is generally not covered unless an additional policy is purchased.

- Maintenance-related issues, such as mold or pest infestations, are usually not covered.

- Choosing the Right Policy:

Selecting the appropriate homeowners insurance policy is crucial. Homeowners should consider the following when evaluating their options:

- Assess personal belongings and their value accurately.

- Understand the policy’s limit and deductibles.

- Compare quotes from different insurers to find competitive rates.

- Review the insurer’s financial stability and customer feedback.

- Benefits of Homeowners Insurance:

The advantages of homeowners insurance extend beyond protection and can include:

- Peace of mind knowing that you have financial backing in case of unforeseen events.

- Potential discounts for bundling with other insurance policies, such as auto insurance.

- Assurance of legal and liability coverage, which can be invaluable in today's litigious landscape.

An Easy Way To Estimate Homeowners Insurance

This visual representation provides a simplified method for estimating homeowners insurance costs, illustrating key factors that impact premiums.

What Does Standard Homeowners Insurance Cover?

This image outlines the core aspects of a standard homeowners insurance policy, emphasizing coverage options and limits.

Homeowners Insurance: Definition, Coverage, Types, Examples

A breakdown of homeowners insurance, defining its significance, coverage types, and some examples to illustrate its use.

Tennessee Homeowners Insurance 101

This resource provides critical information specifically related to homeowners insurance in Tennessee, addressing unique risks and coverage requirements in the state.

Florida Homeowners Insurance

An overview of homeowners insurance considerations specific to Florida, highlighting challenges posed by natural disasters like hurricanes.

Generating Homeowners Insurance Leads

This image explores strategies for generating leads in the homeowners insurance market, emphasizing the importance of diverse marketing approaches.

Understanding homeowners insurance goes beyond merely purchasing a policy. Homeowners should actively engage in evaluating their coverage needs, understanding how claims work, and remaining informed about changes in insurance laws and markets. Regularly revisiting their insurance and making necessary adjustments ensures they maintain adequate coverage over time.

1. Question: What are the key components that make up a typical homeowners insurance policy?

The key components that make up a typical homeowners insurance policy include dwelling coverage, which protects the structure of the home; personal property coverage, which safeguards belongings within the house; liability coverage, designed to protect against legal liability for injuries or damages; and additional living expenses coverage, which covers costs if the home is uninhabitable due to a covered event.

2. Question: How can homeowners reduce their homeowners insurance premiums?

Homeowners can reduce their homeowners insurance premiums by increasing their deductibles, bundling insurance policies with the same insurer, improving home security features, maintaining a good credit score, and regularly reviewing and adjusting their coverage needs to avoid over-insuring.

3. Question: Why is it crucial for homeowners to regularly review their insurance policies?

It is crucial for homeowners to regularly review their insurance policies to identify changes in the value of their property and belongings, to account for any new risks that may arise, to ensure their coverage reflects current market conditions, and to take advantage of potential discounts or favorable changes in the insurance market.

In conclusion, homeowners insurance is a fundamental aspect of homeownership that requires careful consideration and ongoing attention. Homeowners should remain proactive in their insurance planning to ensure they are adequately protected against potential risks.